If you've ever read a book about investing, you've probably heard the same advice: buy a low-cost index fund, hold it forever, and don't touch it. It's simple. Decades of evidence back it up. It works most of the time.

But what happens when "most of the time" isn't good enough?

Buy-and-hold is a great starting point, but it's not the full picture. Market crashes expose its weaknesses. Most people fail at staying the course. A rules-based tactical system can act like a seat belt for your portfolio.

The Buy-and-Hold Revolution

Let's give credit where it's due. Buy-and-hold, popularized by Vanguard founder Jack Bogle, was a genuine revolution in personal finance.

Index funds didn't exist for most of market history. People paid expensive fund managers to pick stocks. Those managers rarely beat the market after fees.

Bogle's idea was simple: don't try to beat the market. Just own the entire market at the lowest possible cost. In The Little Book of Common Sense Investing, he showed that the average actively managed fund underperforms a simple index fund over time. Fees and trading costs explain most of the gap.

This advice is sound. Over the long run, the U.S. stock market has returned roughly 10% per year before inflation. If you're 25, putting money into an index fund and not touching it for 40 years is a perfectly reasonable strategy.

But here's the catch: not everyone has 40 years. And the people who do aren't robots.

What Actually Happens During a Crash

Buy-and-hold sounds easy when markets are going up. But markets don't always go up. Let's look at three major crashes and what they actually meant for real investors.

The Dot-Com Crash (2000–2002)

- The S&P 500 fell 49% from peak to trough.

- It took over 7 years to recover to its previous high (not until October 2007).

- The tech-heavy Nasdaq lost 78% and didn't recover for 15 years.

The Global Financial Crisis (2007–2009)

- The S&P 500 fell 55% from peak to trough.

- $100,000 invested at the peak became roughly $45,000 at the bottom.

- It took about 5.5 years to return to the prior high (March 2013).

The 2022 Bear Market

- The S&P 500 fell about 24% from its January peak.

- Bonds, often the "safe" part of a portfolio, fell about 13% too. That was their worst year in decades.

- A classic 60/40 stock-bond portfolio lost about 17%. The traditional "diversified" strategy failed to protect investors.

Source: scrab.com

Here's what these numbers mean in plain English: if you retired in 2000 or 2007 and planned to live off your investments, you would have watched half your life savings evaporate. "Just hold on" is easy advice to give. It becomes devastating to follow when your mortgage depends on it.

📚 Robert Shiller, the Nobel Prize-winning economist, warned about overvaluation before the 2000 and 2008 crashes in his book Irrational Exuberance. His research showed that stock prices far ahead of actual company earnings lead to painful corrections. Markets aren't always rational, and crashes aren't random bad luck.

The Emotional Cost: Why "Stay the Course" Doesn't Work

This is where buy-and-hold runs into its biggest problem. It's not about math. It's about people.

Every year, a research firm called Dalbar publishes a study measuring how the average investor actually performs compared to the market. The results are consistently dismal:

- Over the 30 years through 2023, the S&P 500 returned about 10.1% per year.

- The average stock fund investor earned only about 6.8% per year.

- That's a gap of over 3 percentage points, every single year.

A 3% gap doesn't sound like much, but compounded over 30 years it's enormous. A $100,000 investment at 10.1% grows to about $1.8 million. At 6.8%, it grows to about $720,000. That's a difference of over a million dollars, all from bad timing decisions.

Why does this happen? Stocks crash, and people panic and sell at the bottom. Stocks soar, and people get excited and buy at the top. It's perfectly human behavior, but it destroys returns.

The brutal irony of buy-and-hold is this: the strategy only works if you actually hold. Decades of evidence show that most people can't, especially when it hurts most.

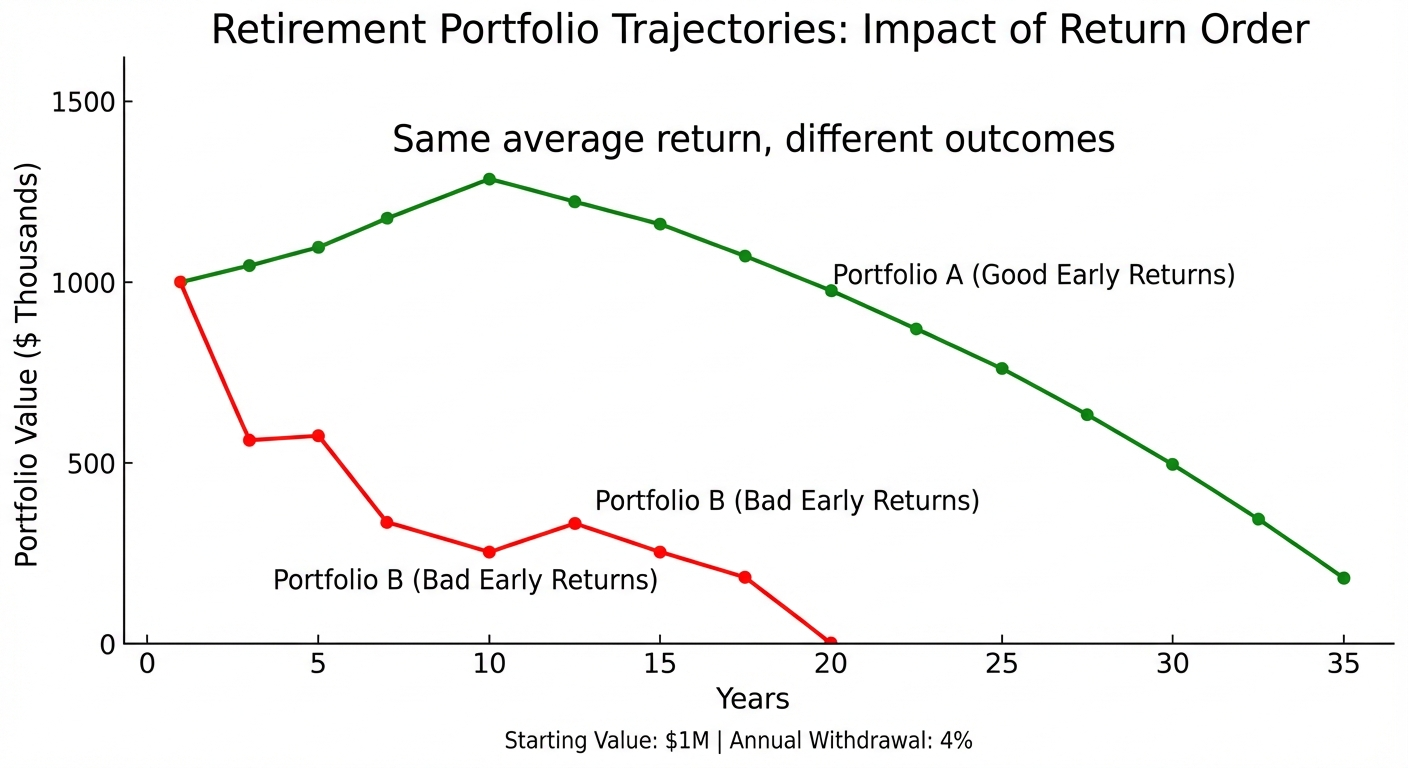

Sequence of Returns: When Timing Matters Even If You Never Sell

There's another problem with buy-and-hold that has nothing to do with emotions. It's called sequence of returns risk, and it matters most for people near or in retirement.

The concept is straightforward. You withdraw money from your portfolio to pay bills. A big drop early in retirement can permanently damage your finances. The market recovers later, but the damage is already done.

Financial planner William Bengen studied this in his landmark 1994 research. He developed what became known as the "4% rule." Retirees can safely withdraw 4% of their savings each year. But that rule assumes a balanced portfolio and a favorable sequence of returns. A major crash in the first few years of retirement can break the plan entirely. You either cut spending or run out of money.

For a 30-year-old, a crash is a buying opportunity. For a 63-year-old about to retire, it's a potential catastrophe.

So What Is Tactical Investing?

Tactical investing is not day trading. It's not trying to predict the future. And it's definitely not watching CNBC and making gut-feel decisions.

Tactical investing means using simple, predefined rules to adjust your portfolio based on market conditions. Instead of always holding 100% stocks, a tactical system shifts some money into safer assets like bonds or cash during downturns. It shifts back during recoveries.

Think of it like driving a car. Buy-and-hold says: "Get on the highway and never touch the brakes." Tactical investing says: "Drive normally, but if you see a storm ahead, slow down."

The key principles of tactical investing:

- Rules-based, not gut-based. Decisions follow clear signals like moving averages or momentum indicators. No hunches. No headlines.

- Infrequent trades. Most tactical strategies check signals monthly, not daily. You're not glued to a screen.

- Risk management, not return chasing. The goal is to avoid the worst losses, not to beat the market every year.

- Backed by research. These aren't trade secrets. They're strategies published in academic journals that anyone can follow.

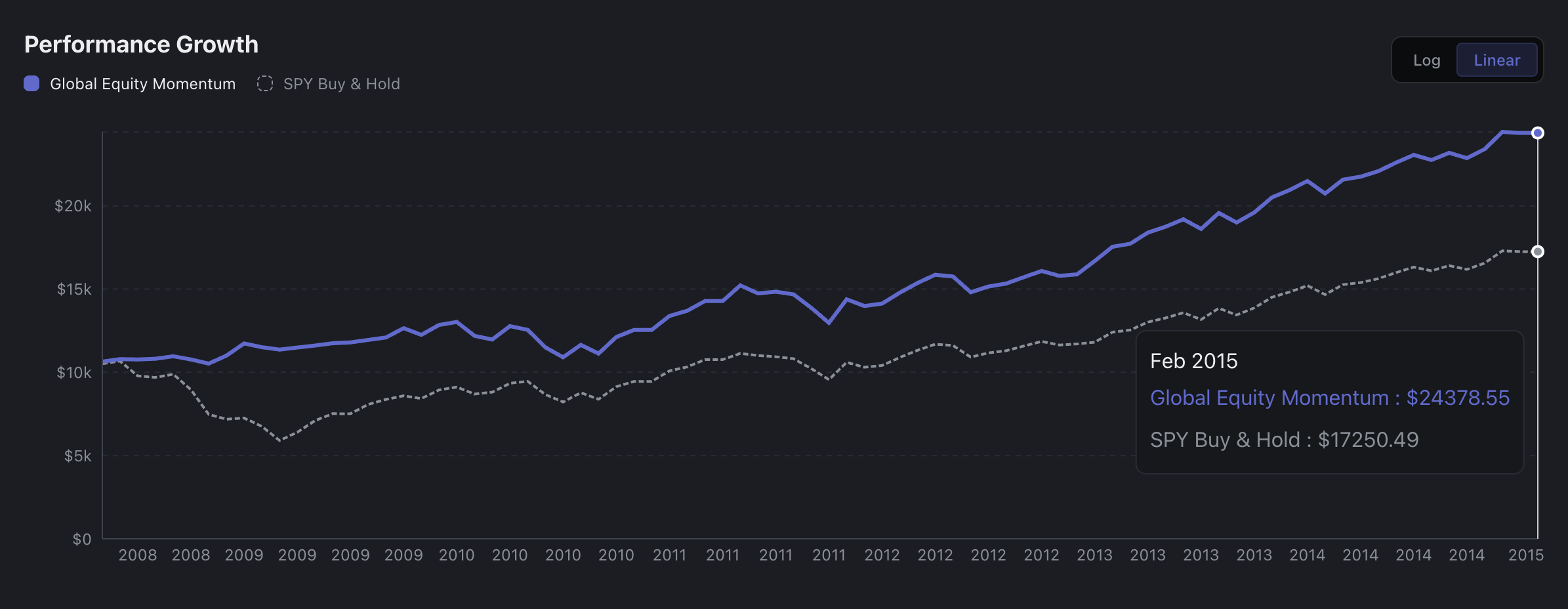

How Tactical Strategies Handled the 2008 Crisis

One of the most cited tactical methods comes from Meb Faber. He published a groundbreaking 2007 paper called "A Quantitative Approach to Tactical Asset Allocation." The idea is deceptively simple:

If the price of an asset is above its 10-month moving average, hold it. If it's below, move to cash or bonds.

That's it. No complicated formulas. No insider information. Just one rule.

Faber tested this strategy going back to the 1970s. The results were striking:

- The strategy delivered similar long-term returns to buy-and-hold.

- But with dramatically lower drawdowns. The worst losses were cut roughly in half.

- During the 2008 crash, the strategy moved out of stocks and into bonds before the worst of the decline. This cut losses sharply.

- It re-entered stocks during the recovery, capturing most of the upside.

📚 Faber's paper found that a simple moving-average rule applied to five asset classes (U.S. stocks, foreign stocks, bonds, real estate, and commodities) reduced the maximum drawdown from over 50% to roughly 20%. Long-term returns stayed competitive.

Why does something this simple work? Big market crashes don't usually happen overnight. They develop over months in a slow, grinding decline. A trend-following rule picks up on this deterioration early enough to step aside before the worst damage hits.

Source: reblnc.com

It's Not About Being Right Every Time

Let's be honest about the trade-offs. Tactical strategies are not magic. They have real costs:

- False signals. Sometimes the market dips, the strategy sells, and the market bounces right back. You get "whipsawed," selling low and buying back higher.

- Lagging in bull markets. During strong, steady uptrends, a tactical strategy will match or slightly trail buy-and-hold. Occasional false exits cause the drag.

- Discipline required. You need to follow the rules even when it feels wrong. Your strategy says "sell" but everyone around you is making money. It takes conviction.

But here's the key point: you don't need to be right every time. You just need to avoid the catastrophic losses.

Here's a simple math fact that surprises most people:

- If your portfolio drops 50%, you need a 100% gain just to get back to where you started.

- If your portfolio drops 20%, you only need a 25% gain to recover.

By limiting losses during the worst periods, tactical strategies make recovery dramatically faster. You give up a small edge in good times. But you spend far less time digging out of deep holes.

The Case for "Buy-and-Hold With a Seat Belt"

We're not here to tell you that buy-and-hold is bad. It's not. It's one of the greatest ideas in personal finance. It works well for many people, especially young investors with long time horizons and the emotional strength to ignore crashes.

But we think there's a better way to frame it:

Buy-and-hold is the engine. Tactical rules are the seat belt. You don't plan to crash, but you still buckle up.

A tactical system gives you:

- Smaller losses during bear markets. Your portfolio doesn't fall as far, so recovery is faster.

- Emotional protection. You have a plan for downturns. You're less likely to panic-sell at the worst time.

- Better retirement outcomes. Reducing sequence of returns risk protects your income when it matters most.

- Competitive long-term returns. The research shows that over full market cycles, tactical strategies keep pace with buy-and-hold, with a much smoother ride.

The best part? You don't need a finance degree or expensive software. The rules are published, the data is freely available, and the process takes about 15 minutes once a month.

Sources & Further Reading

- Faber, M. (2007). "A Quantitative Approach to Tactical Asset Allocation." The Journal of Wealth Management. — The foundational paper for trend-following tactical strategies using simple moving averages.

- Shiller, R. (2000). Irrational Exuberance. Princeton University Press. — Nobel laureate's analysis of market bubbles and why stock prices can depart from fundamentals for extended periods.

- Dalbar Inc. Quantitative Analysis of Investor Behavior (QAIB). Annual study. — The definitive annual research on the gap between market returns and the returns actually earned by average investors.

- Bogle, J. (2007). The Little Book of Common Sense Investing. Wiley. — The classic case for low-cost index investing and the buy-and-hold philosophy.

- Bengen, W. (1994). "Determining Withdrawal Rates Using Historical Data." Journal of Financial Planning. — The original research behind the "4% rule" for retirement withdrawals, highlighting sequence of returns risk.

- S&P 500 historical drawdown data via Standard & Poor's / Macrotrends — Historical price data used for drawdown and recovery calculations referenced in this article.

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.